In the age of digital transformation, data has become a valuable asset for organizations. However, sharing this data securely and efficiently remains a challenge. Traditional methods of data sharing are often slow, expensive, and vulnerable to cyber threats. But what if there was a technology that could revolutionize the way we share data? Enter blockchain. In this blog post, we’ll explore the role of blockchain in organizations and how it’s changing the game when it comes to data sharing. Get ready to discover a new era of secure and transparent information exchange.

Understanding Blockchain Technology: A Brief Overview

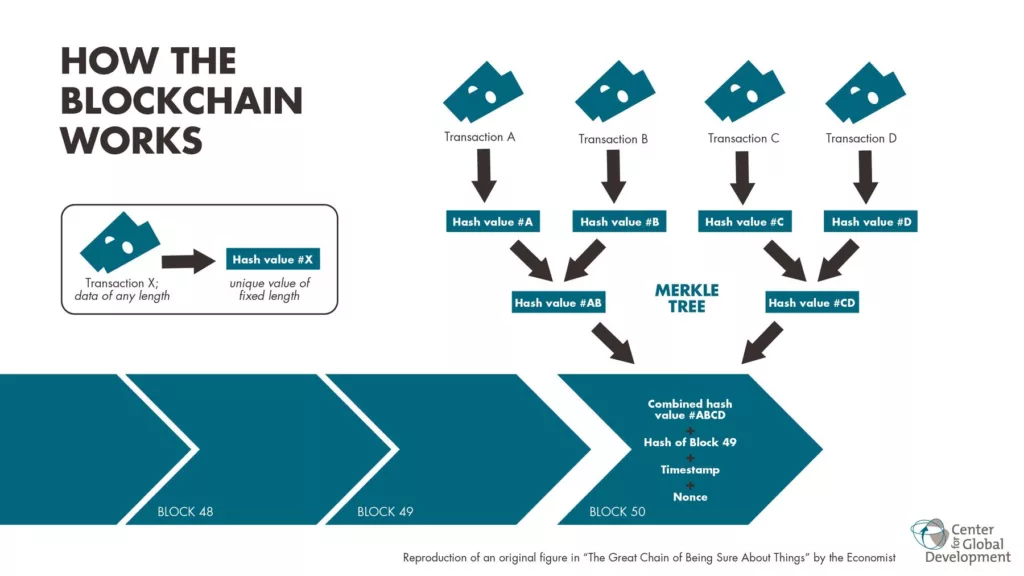

Blockchain technology has become a buzzword in recent years, but not everyone understands what it is and how it works. Essentially, blockchain is a decentralized digital ledger that records transactions between different parties using secure cryptographic algorithms. This means that there is no need for intermediaries such as banks or payment processors to verify the legitimacy of transactions. Instead, each transaction is verified by multiple nodes on the network, making it virtually impossible to tamper with or hack.

One of the key features of blockchain technology is its ability to promote transparency and trust in data sharing processes. By creating an immutable record of all transactions on the network, organizations can be sure that their data cannot be altered without permission or knowledge. Additionally, blockchain allows for greater control over who has access to sensitive information, since permissions can be granted and revoked by authorized parties at any time.

Overall, understanding the basics of blockchain technology lays down the foundation for exploring its potential benefits when used within organizational contexts.

The Benefits of Blockchain Technology for Data Sharing in Organizations

Blockchain technology has emerged as a game-changer for organizations looking to share data securely and efficiently. One of the key benefits of blockchain is its ability to provide transparency and immutability, which means that once data is added to the blockchain, it cannot be altered or deleted. This makes it an ideal solution for organizations that need to share sensitive information with multiple parties while ensuring that the data remains secure and tamper-proof.

Another advantage of blockchain technology is its ability to streamline processes and reduce costs associated with traditional methods of data sharing. By eliminating intermediaries and automating processes, organizations can save time and money while improving the overall efficiency of their operations.

Overall, blockchain technology offers a range of benefits for organizations looking to share data securely and efficiently. From increased transparency and immutability to streamlined processes and cost savings, it’s clear that blockchain is revolutionizing the way organizations approach data sharing.

How Blockchain Technology is Revolutionizing Data Sharing in Organizations

Blockchain technology is transforming the way organizations share data. Unlike traditional systems that rely on intermediaries to verify transactions, blockchain allows for a decentralized network where all parties have access to the same information in real-time.

This immediacy and transparency eliminate the need for costly and time-consuming manual processes, thus increasing efficiency. Additionally, blockchain’s immutable ledger ensures data accuracy, as changes can only be made via consensus agreement by members of the network.

Another important benefit of blockchain technology in data sharing is its increased security. The system uses advanced cryptography techniques to protect against fraud and hacking attempts in real-time. This enhanced security also helps build trust among users, making it easier to do business with each other without fear of fraudulent activities.

Overall, blockchain technology has significant potential when it comes to revolutionizing data sharing practices within organizations. From enhancing efficiency and transparency to improving security through cryptographic techniques – adopting this new innovation could prove invaluable for your organization’s digital transformation strategy.

The Role of Blockchain in Enhancing Data Security and Privacy

Blockchain technology plays a crucial role in enhancing data security and privacy for organizations. With its decentralized nature, the blockchain eliminates the need for intermediaries and creates a tamper-proof digital ledger that records all transactions securely. The use of cryptography ensures that data is encrypted and only accessible to authorized parties with private keys, providing an added layer of protection against cyber attacks.

Moreover, blockchain technology allows for transparent and auditable data sharing, enabling organizations to track every interaction on the network without compromising sensitive information. This ability to maintain transparency while protecting privacy makes blockchain ideal for industries such as healthcare, finance, and supply chain management where trust is paramount.

By using blockchain technology in their data sharing processes, businesses can significantly reduce risks associated with unauthorized access or manipulation of data by malicious actors. Additionally, blockchain provides an immutable record of all interactions within the network that can be used in cases of dispute resolution or auditing purposes.

Real-World Examples of Organizations Using Blockchain for Data Sharing

How IBM Is Using Blockchain for Data Sharing Across Different Industries

IBM is using blockchain technology to revolutionize data sharing across different industries. One of their notable projects is the Food Trust, which uses blockchain to track the origin and journey of food products from farm to table. This ensures transparency and accountability in the food supply chain, reducing the risk of foodborne illnesses and increasing consumer trust. Another example is TradeLens, a blockchain-based platform for global trade that connects shippers, freight forwarders, and customs officials to streamline processes and reduce paperwork. These real-world examples demonstrate how blockchain technology can improve data sharing in organizations by providing secure, transparent, and efficient solutions.

Case Study: Walmart’s Successful Implementation of Blockchain in Supply Chain Management

Walmart has successfully implemented blockchain technology in supply chain management, enabling the tracking of food products from farm to store. The use of decentralized ledgers allows for greater transparency and efficiency in the supply chain, reducing the time it takes to track a product’s origin and ensure its safety. This system has been particularly useful when tracing food-borne illnesses to their source and recalling contaminated products quickly. Other companies such as IBM have also utilized blockchain technology in logistics management, demonstrating how this innovative tool can transform industries beyond just finance or tech.

Enhancing Healthcare Coordination and Data Security with Blockchain: A Look at Startup Gem

Gem, a startup based in Los Angeles, is revolutionizing the healthcare industry by using blockchain technology to enhance coordination and security of patient data. The company’s platform allows healthcare providers to securely share sensitive information such as medical records and insurance claims with each other without compromising confidentiality. Gem’s solution enables patients to have complete control over their health data ownership and privacy while streamlining the communication between different healthcare providers. By utilizing decentralized ledger technology, Gem ensures that all parties involved can access and update information in real-time while preventing any unauthorized access or tampering of critical patient data. This innovative approach highlights how blockchain improves data security and enhances coordination for organizations in highly regulated industries like healthcare.

Realizing the Benefits of Decentralized Finance through Blockchain-based Data Sharing

Decentralized finance (DeFi) is one of the most promising applications of blockchain technology in the financial sector. By leveraging blockchain-based data sharing, DeFi platforms can provide users with greater financial autonomy and transparency. For instance, Aave, a decentralized lending platform, uses blockchain to enable peer-to-peer lending without intermediaries. Another example is Uniswap, a decentralized exchange that allows users to trade cryptocurrencies without relying on centralized exchanges. These platforms are able to achieve greater efficiency and security by utilizing blockchain technology for data sharing. As more organizations explore the potential of DeFi and other blockchain-based applications, we can expect to see even more innovative use cases for this transformative technology.

The Future of Data Sharing: How Blockchain is Shaping the Landscape

Real-World Examples of Organizations Using Blockchain for Data Sharing

Blockchain technology has already made a significant impact on data sharing in various industries. For instance, Walmart has implemented blockchain to track the origin of food products, which has helped to improve food safety and reduce waste. Another example is the financial industry, where blockchain is being used to facilitate secure and transparent transactions between banks and other financial institutions.

In the healthcare sector, blockchain is being used to improve patient data management and sharing. The MedRec project, for example, uses blockchain to create a decentralized medical record system that allows patients to control their own data and share it securely with healthcare providers.

Other industries that are exploring the use of blockchain technology for data sharing include supply chain management, energy, and government. These real-world examples demonstrate the potential of blockchain to revolutionize data sharing in organizations across various sectors.

Exploring the Challenges and Limitations of Blockchain for Data Sharing in Organizations

Scalability Issues: Can Blockchain Keep Up with the Data Demands of Organizations?

One challenge of implementing blockchain technology for data sharing in organizations is scalability. While the decentralized nature of blockchain ensures security and tamper-proof data transactions, it can also lead to slower processing times compared to traditional centralized systems. As more data is added to the network, the processing power required increases as well, leading to potential scaling issues. Improvements such as sharding and off-chain solutions are being developed to address this concern; however, organizations must weigh the benefits against these scalability challenges and consider if a hybrid solution may be necessary for their specific needs.

Security Concerns: How Vulnerable is Blockchain to Cyber Attacks and Data Breaches?

While blockchain technology is highly secure, there are still security concerns that organizations need to be aware of. One major concern is the risk of cyber attacks and data breaches on the platforms used to access blockchain networks. While attacks on the actual blockchain network are unlikely due to its decentralized nature, hackers may target endpoints such as wallets or exchanges for their personal gain. Therefore, it’s important for organizations to invest in strong endpoint security measures and ensure all users properly protect their digital assets. Additionally, regular vulnerability assessments and updates should be conducted to minimize any potential risks associated with using blockchain technology for data sharing purposes.

Interoperability Challenges: Can Blockchain be Integrated with Existing Data Sharing Systems in Organizations?

Interoperability challenges pose a significant obstacle to integrating blockchain technology with existing data sharing systems in organizations. Legacy systems that have been in place for years may not be compatible with blockchain, requiring costly upgrades or replacements. Additionally, standardization of blockchain protocols is still lacking, making it difficult for different blockchains to communicate with each other. As a result, organizations may need to invest in additional resources and expertise to ensure seamless integration. However, as blockchain technology continues to evolve and gain wider adoption, interoperability challenges are expected to be addressed through the development of industry standards and protocols.

Regulatory Hurdles: How Will Government Regulations Impact the Adoption of Blockchain for Data Sharing in Organizations?

The use of blockchain technology presents regulatory challenges for organizations. The lack of a clear legal framework governing blockchain has created uncertainty around issues such as data privacy, intellectual property rights, and liability. Additionally, some government regulations may conflict with the decentralized nature of blockchain. For example, certain financial regulations require centralized control and oversight.

Furthermore, compliance with international regulations can be particularly challenging given the global reach of blockchain networks.

Overall, while the potential benefits of using blockchain for data sharing are clear, organizations must navigate through a complex regulatory landscape to ensure they comply with relevant laws and standards. Effective collaboration between industry stakeholders and regulators is key to addressing these challenges and facilitating widespread adoption.

Best Practices for Implementing Blockchain Technology in Your Organization

Implementing blockchain technology in your organization can be a complex process, but there are some best practices that can help ensure a successful implementation. One important key phrase to keep in mind is “start small.” It’s important to begin with a small pilot project to test the technology and identify any potential issues before scaling up. Another key phrase to consider is “collaborate with stakeholders.” Involve all relevant stakeholders in the planning and implementation process, including IT, legal, compliance, and business teams. This will help ensure that everyone is on board with the project and that any concerns or challenges are addressed early on. Other best practices include selecting the right blockchain platform for your needs, ensuring data quality and accuracy, and providing adequate training for employees. By following these best practices, your organization can successfully implement blockchain technology for data sharing.

How to Ensure Compliance and Regulatory Requirements When Using Blockchain for Data Sharing

When using blockchain for data sharing, it’s important to ensure compliance with regulatory requirements. Data privacy regulations such as the General Data Protection Regulation (GDPR) must be considered when implementing blockchain technology. Organizations should also consider any industry-specific regulations that may apply, such as those in healthcare or finance. It’s recommended to work closely with legal experts when considering the use of blockchain technology for data sharing and storage to ensure compliance. Another important consideration is ensuring that all participants in a blockchain network are properly identified and authenticated, preventing unauthorized access to sensitive data. By carefully addressing compliance and regulatory concerns, organizations can reap the benefits of secure and transparent data sharing through blockchain technology while remaining within legal boundaries.

Conclusion: Why Your Organization Should Consider Adopting Blockchain for Data Sharing

Revolutionize data sharing in your organization today by embracing blockchain technology. The benefits are clear: enhanced security, improved transparency, and reduced costs. By leveraging blockchain’s decentralized network, organizations can streamline their data-sharing processes while ensuring the privacy of sensitive information. From supply chain management to healthcare records, there are countless applications for blockchain in data sharing.

As we move towards a more digital world where data is king, it becomes increasingly important for organizations to adopt new technologies that keep them ahead of the curve. Blockchain is quickly becoming one of those essential technologies. Don’t get left behind – start exploring how blockchain can transform your organization’s approach to data sharing today!

In conclusion, blockchain technology has revolutionized the way organizations share data. It provides a secure and transparent way of sharing information while ensuring privacy and reducing the risk of data breaches. The benefits of blockchain technology for data sharing are numerous, and organizations that adopt this technology stand to gain a competitive advantage in their respective industries.

However, implementing blockchain technology is not without its challenges and limitations. Organizations must be aware of these limitations and best practices to ensure successful implementation.

If you’re interested in learning more about how blockchain technology can benefit your organization, be sure to check out our other content on the topic. We provide valuable insights and practical tips for implementing blockchain technology in your organization. Don’t miss out on this opportunity to stay ahead of the curve in data sharing and security.